Did you know you can get the Sprott Money Monthly Wrap Ups, Ask The Expert,

special promotions and insightful blog posts sent right to your inbox?

Sign up to the Sprott Money Newsletter here.

In this blog, we delve into the concept of short squeezes and their potential impact on the price of silver.

By now, most everyone understands that the bullion bank trading desks freely manage and manipulate COMEX precious metal prices. But they don't just move price to the downside. The banks will also manipulate prices higher if there is profit to be made. They did so on four occasions in late 2022 and they appear to be setting the table for another spec short squeeze in the near future.

Understanding Silver Price Manipulation and Short Squeezes

Let's start with the current situation. As the value of the U.S. Dollar Index fell sharply in July, speculator and hedge fund cash rushed into COMEX silver. In just one five-day period mid-month, the dollar index fell by nearly two full points from near 102 to below 100. The hedge funds responded by aggressively buying COMEX silver contracts and the silver price rallied by over $2.00 or about 8.5%.

You can see this on the chart below from the CFTC's Commitment of Traders report. This data was published on Friday, July 21, and it reveals the position changes during the reporting week of Wednesday, July 12 through Tuesday, July 18.

Note that, over the period of July 12-18, the swap-dealing banks dumped 1,137 longs while adding 14,768 new shorts. In contrast, the speculating hedge funds covered 1,932 shorts while adding a whopping 22,259 new longs. Again, it was this massive net speculator buying of COMEX silver contracts that drove the price higher by over $2 during the period.

As you're likely aware, the three weeks since that event have brought a turnaround in the dollar index, and it has rallied nearly three full points. In turn, the speculating hedge funds have rushed to sell all of those COMEX silver contracts that they were gleefully and blindly buying three weeks earlier.

The next set of data that you see below is from last week's Commitment of Traders report for the period of Wednesday, August 2 through Tuesday, August 8. Over just those five days, the COMEX silver price fell by $1.52/ounce, while the Dollar Index rallied about a full point.

Look at what was taking place... the exact opposite of three weeks earlier. The banks added 383 new longs while covering 12,452 of their shorts. The hedge funds dumped 12,593 of their longs and added 3,846 new shorts.

Do you see how this works? OK, good. Now to the point of this post.

Let's scroll up and do some math. On that first CFTC report, note that the hedge funds were NET LONG 29,689 COMEX silver contracts (subtract the gross short position from the gross long position). Now three weeks later, and with the price about 10% lower, those same funds are NET SHORT 3,781 contracts. Is this important? YES! Because if the banks are willing to take the short side against the hedge funds before a price plunge, they're also happy to take the long side against those same funds before price rallies in a short squeeze.

Keeping a Vigilant Eye on Silver Price Trends and Market Behavior

As you're about to see, this squeezing of the spec hedge fund shorts happened four times late in 2022, and all of the squeezes came about following periods where the hedge funds had collectively built massive short positions.

On the chart below from late 2022, you'll notice four very quick spec short squeezes. I've numbered them 1-4 so that you can easily spot them.

And what was the Commitment of Traders data before each squeeze?

Short Squeeze #1 began on Tuesday, July 26. Since it was a Tuesday, there was a Commitment of Traders survey taken at the COMEX close. Note that as of that day – and just before a 12.2% price spike occurred – the banks were NET LONG 14,560 COMEX silver contracts while the hedge funds were NET SHORT 17,818 contracts.

By the following Tuesday, the cause of the 12% rally was revealed. Note that the hedge funds had covered 12,656 of their shorts and it was all of that buying to cover that drove the price rally.

Next came Short Squeeze #2. After that July rally fizzled out on August 15, the price bottomed again on Thursday, September 1. There was a Commitment of Traders survey taken on Tuesday, August 30 – and what did it reveal? The hedge funds were massively NET SHORT again, this time to the tune of 21,031 COMEX silver contracts. What happened next? A 15% rally/spike in six days.

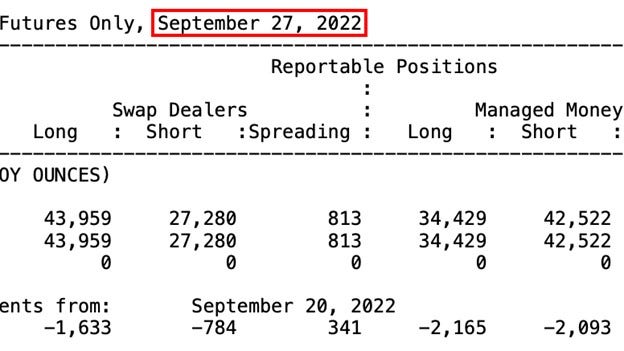

Obviously, those hedge fund managers are slow learners, not very bright and naive enough to think that they have a chance against the bullion bank trading desks. By Tuesday, September 27, they had already been squeezed twice, but they had rebuilt their NET SHORT position to over 8,000 contracts. Guess what happened next? Short Squeeze #3, and this time it was the biggest one yet, as COMEX silver spiked 19.1% in just five days!

Those bank desks were having so much fun making easy money and filling their year-end bonus pools that they must have figured they'd keep crushing the hedge funds as long as the funds were willing to keep playing. And so, on Thursday, November 3, Short Squeeze #4 began. It unfolded over eight days for $3.38, or about 18%. This time, let's dial the report back to the survey date of October 18, as the price was bottoming that day and then moved sideways for a few days before the squeeze began. What do you suppose it revealed? Another mad rush into the short side by the hedge funds leaving the banks NET LONG and the funds NET SHORT.

Navigating the Silver Price Short Squeeze Landscape

So, my hope is that you can see the pattern here. The hedge funds rush in and get NET LONG before price pullbacks, and these same funds rush in and get NET SHORT before price gets squeezed higher. Now that you understand the history, let's look to the future. Here again is that Commitment of Traders data from last week, surveyed on Tuesday, August 8:

The swap-dealing banks are only NET LONG 499 contracts, while the hedge funds are only NET SHORT 3,781. While this is a major shift from just three weeks ago, the positioning is not yet at the levels that preceded all four of those 2022 short squeezes. However, IF price continues to drift lower and IF you see that the hedge funds are continuing to pile into the short side of COMEX silver, you should be ready to take action ahead of the next short squeeze that will inevitably follow.

Don’t miss a golden opportunity.

Now that you’ve gained a deeper understanding about gold, it’s time to browse our selection of gold bars, coins, or exclusive Sprott Gold wafers.

About Sprott Money

Specializing in the sale of bullion, bullion storage and precious metals registered investments, there’s a reason Sprott Money is called “The Most Trusted Name in Precious Metals”.

Since 2008, our customers have trusted us to provide guidance, education, and superior customer service as we help build their holdings in precious metals—no matter the size of the portfolio. Chairman, Eric Sprott, and President, Larisa Sprott, are proud to head up one of the most well-known and reputable precious metal firms in North America. Learn more about Sprott Money.

Learn More

You Might Also Like:

Looks like there are no comments yet.