Did you know you can get the Sprott Money Monthly Wrap Ups, Ask The Expert,

special promotions and insightful blog posts sent right to your inbox?

Sign up to the Sprott Money Newsletter here.

The biggest story of 2023 is not a function of IF the Fed will pause and then pivot to rate cuts. Instead, it's a matter of WHEN will this shift take place. This monetary policy change is coming, and it's actually much closer than you think.

And, obviously, this is the key to gold prices as the year progresses. As long as the Fed keeps hiking—and is expected to continue hiking—the COMEX gold price is unlikely to sustain any moves to the upside. However, as history has taught us, once the Fed shifts back to easing, the gold price will rally. The question on your mind should be: when will this shift occur?

To that end, some important signals are flashing. Let's start with a chart I found on Twitter. Below you'll see the trend of money supply growth in the United States. Money supply growth is important, and it's necessary, too, as an essential component for servicing the existing debt.

Note that year-over-year money supply growth has only contracted on a few occasions over the past 150 years. You might further note that each contraction was rapidly followed by some sort of economic calamity. Are the current bank failures just the first coal mine canaries?

Next, let's revisit our post from last week. In that article, I tried to demonstrate something that's very important about the yield curve. Yes, the inversion of the yield curve is a perfect predictor of an upcoming recession, but the inversion itself does not tell you when the recession will begin. For that, we have to wait for the inversion to begin "uninverting" or flattening. As you can see on the chart below, the expected recession begins shortly after the curve begins to uninvert.

And what has happened in the past week? Driven by the current banking crisis, treasury yields have moved sharply lower but not evenly. Last week, the yield on the U.S. 2-year note hit 5.09%. At the same time, the yield on the U.S. 10-year note was at 4.01%. That made the inversion a whopping 108 basis points and the widest since 1981.

But that was likely the worst of it. Treasuries have since rallied and yields have fallen sharply, particularly on the short end. On Monday of this week, the yield on the 2-year note was all the way back to 3.98% while the yield on the 10-year note was at 3.46%. If you do the math, that's an inversion of just 52 basis points or less than half of what it was just one week ago!

Now look again at that FRED chart posted above. Is the U.S. now on the doorstep of recession if not already immersed in one? This move in the yield curve would certainly seem to suggest it.

Lastly, let's discuss the supposedly "robust" U.S. jobs market. It is this alleged job market "strength" that the Fed is using to justify its dreams of an economy that is resilient in the face of their unprecedented rate hikes. However, the Fed's optimism is misplaced and incorrect, and I think we can connect the data dots to show why.

At present, the Fed is seemingly enamored with the absolute number of jobs alleged to be created each month and then reported by the BLS. For February, this reported total of "new jobs" was 311,000. However, almost all of the jobs that were added over the past 12 months have been part-time jobs—not the higher-quality, salaried, and full-time jobs you'd expect in a strong economic environment.

And why would this be? Because corporate layoffs are surging and workers are desperate to take multiple part-time jobs in order to replace their lost income.

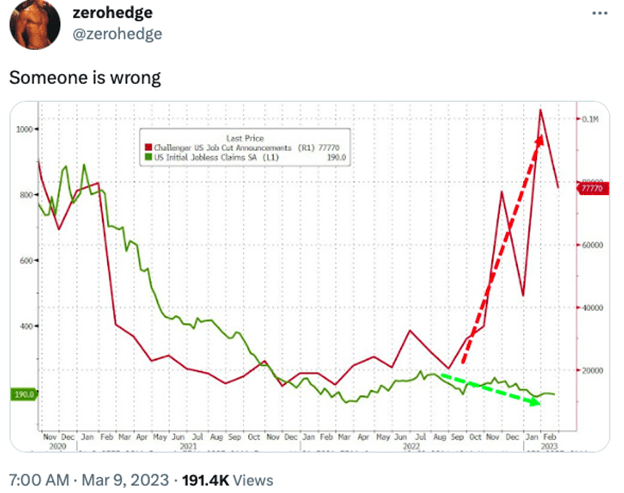

Now here's the thing that the Fed is missing with their backward-looking data analysis. When you get laid off or "downsized" from your corporate job—the one with health insurance benefits and paid time off—you typically get some sort of severance package. Which is nice. However, in the U.S., a person cannot file for unemployment compensation until that severance package pays out.

Stated another way, as long as you're on your severance pay, you can't file a first-time unemployment claim. So now when we plot the layoff data along with the first-time jobless claims data, we get the chart below:

I hope I haven't confused you with this, but if I have, let's cut to the chase.

- The Fed thinks the job market is robust when, in fact, the only jobs being created are of the part-time variety.

- The Fed also thinks that the job market is robust because initial jobless claims have remained low when, in fact, claims are only low due to severance packages, and once these packages end, jobless claims will surge.

- The Fed thinks they can continue to hike rates because the U.S. economy is robust when, in fact, it's weakening by the day and on the edge of a sharp contraction and recession.

At present, and after the bank failures of the past week, odds of a fed funds rate hike have been tumbling, and as such, gold prices have rallied. However, "the market" still believes that the Fed will hike twice more before pausing and pivoting later this year.

What "the market" is missing is that the U.S. economy is likely already in recession and the recession is only going to worsen in the months ahead. The Fed waited too long to hike rates in 2022, foolishly believing that the surging price inflation was "transitory". They are now waiting too long to cut rates, foolishly believing that the U.S. economy remains "robust".

As the dust begins to settle later this year and the full scope of the Fed's economic damage is realized, the Fed will begin cutting rates much faster than most expect. Already, the Fed funds futures market is pricing in as much as 75 basis points of fed funds cuts before year end. That's not enough. Its cuts will be greater than that.

For just as the Fed waited too long to move last year and then responded with the series of unprecedented, 75 basis point rate hikes, the worsening banking crises and a faltering economy will force them to sharply cut rates later this year. The yield curve and the latest data seems to suggest that this is a foregone conclusion.

As this pertains to the gold price, what you saw in January—and what you've seen over the past week—is just a hint of what's to come. History has shown that Fed easing cycles are coincident with a rising gold price. See 2010-2011 and 2019-2020 as your most recent examples. The period of 2023-2024 is very likely to repeat the pattern.

Don’t miss a golden opportunity.

Now that you’ve gained a deeper understanding about gold, it’s time to browse our selection of gold bars, coins, or exclusive Sprott Gold wafers.

About Sprott Money

Specializing in the sale of bullion, bullion storage and precious metals registered investments, there’s a reason Sprott Money is called “The Most Trusted Name in Precious Metals”.

Since 2008, our customers have trusted us to provide guidance, education, and superior customer service as we help build their holdings in precious metals—no matter the size of the portfolio. Chairman, Eric Sprott, and President, Larisa Sprott, are proud to head up one of the most well-known and reputable precious metal firms in North America. Learn more about Sprott Money.

Learn More

You Might Also Like:

Looks like there are no comments yet.